NeutraHealth

Aimzine is a FREE online magazine for investors and everyone involved with AIM companies. If you are not already registered to read Aimzine please click here

An Update on a Previously Featured Company

If you purchase own-brand vitamins from a supermarket or major healthcare chain there is a very good chance that you will buying a product manufactured by Brunel Healthcare, a wholly owned subsidiary of NeutraHealth. Amongst others, Brunel supplies Tesco, Sainsbury’s, Boots and Superdrug.

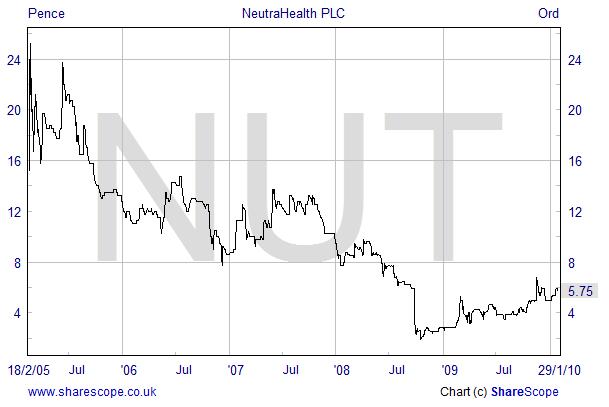

Aimzine first covered NeutraHealth in November 2008. In our original article we commented that NeutraHealth’s shares had been ‘particularly harshly treated’ following a profits warning. Since that time the share price has recovered from 2.6 pence to 5.4 pence. However, NeutraHealth’s shares were once multiples of this level. So, could there be scope for further progress here? I met with Finance Director, Robin Hilton to gain a better understanding of the Group’s prospects today.

Raw Materials

Robin explained that NeutraHealth has experienced difficulties over the last 18 months which have slowed growth, but throughout this period the Group has remained profitable. Their biggest problem has been the volatility in the price of their raw materials - rising input prices have a direct impact on profits. Take, for example, the price of Vitamin C. Most of the world’s supply of this vitamin is sourced from China. In 2008, at the time of the Beijing Olympics, the supply was disrupted and the raw material price rocketed from £2.50 to £13 per kilogram. It had been expected that prices would fall away once the Olympics were complete, but today the price is still at £8 per kilogram. Problems with raw material prices have been exacerbated by a weak pound.

NeutraHealth is focused on improving input prices and is working with suppliers to build better relationships. For example the Group has recently concluded a new agreement with a major supplier of glucosamine, which will provide greater transparency of pricing. Glucosamine, produced from crushed oyster shells, is used by arthritis sufferers.

Most of the world's supply of vitamin C is from China

NeutraHealth serves the private label multiple retail sector through its Brunel subsidiary. Brunel is performing well with increasing turnover and is seeking to become the minimum cost supplier as it pursues ‘factory gate’ prices. In this sector NeutraHealth is also making progress with innovative new products which has resulted in more product listings.

Biocare and the Group’s other businesses are focussed on practitioner, independent, and direct to consumer channels. These higher margin channels have not performed as strongly in 2009 as the Brunel business. However, Robin Hilton is very optimistic about prospects for these businesses going forward. Robin explains that market research and a new computer system are proving extremely useful in returning this area to a growth path.

In a Trading Statement issued on 21 January, NeutraHealth indicated that trading for 2009 was in line with expectations. The forecasts, from the house broker Cenkos, are shown in the table below.

Year to 31st December

|

2007 |

2008 |

2009 (forecast) |

2010 (forecast) |

Revenue (£ million) |

21.31 |

28.86 |

34.00 |

37.50 |

Pre tax profit (£ million) |

2.10 |

1.00** |

1.40 |

1.80 |

Earnings per share (pence) |

0.95 |

0.40 |

0.58 |

0.72 |

** Excludes £1 million exceptional profit

The Trading Statement reported: ‘Sales in the second half of 2009 were strong, and are expected to exceed £18 million. This is almost 9% growth on the first six months of 2009, and over 4% growth on the second half of 2008. This has been achieved through product innovation and by focusing on our core customers, which has led to an increase in consumer demand. ‘

The 21 January RNS also reported the sale of a small loss-making subsidiary, Nutrigold. Cash received on disposal was £315,000. The statement indicated that there will be a non-cash goodwill impairment charge for Nutrigold in the 2009 results.

Until conditions deteriorated, NeutraHeath were keen to made further acquisitions. However, economic conditions and a low share price make further purchases unlikely – at least in the short term. Instead the Group is focussing on organic growth.

The Group are optimistic that current initiatives, such as the work on innovative new products and the focus on reducing input costs, will drive growth and improve profitability. Robin Hilton believes that, over time, there is scope to make considerable improvements to operating margins. Furthermore, he is hopeful that the Group will be able to start paying dividends in the not too distant future.

Aimzine Comment

NeutraHealth shares have performed very well over the last year. However, even after this considerable improvement, the shares trade on a current year p/e of just under 8.

Trading is good, but not quite ‘exciting’ and perhaps the share suffers from the lack of any obvious prospect of near-term drivers. Nonetheless, we believe NeutraHealth to be a business worth following. There seems to be a lot of promising initiatives underway, which, over time, should drive growth and profitability.

In February 2009 NeutraHealth received an unsolicited approach from its largest shareholder, Elder Pharmaceuticals of India. Elder considered increasing its shareholding from 21% to around 55% and indicated that it might offer 5.5 pence per share in cash to shareholders to facilitate the increase in holding. Elder finally stated at the end of July 2009 that, on consideration, they had no intention of making an offer at that time.

We cannot say whether Elder will revive their interest in increasing their stake in NeutraHealth at some stage. However, we can understand that a predator may find NeutraHealth of interest. The shares are on a low rating and yet NeutraHealth are a profitable Group with scope for growth and improvements in profitability. Furthermore, NeutraHealth has a most impressive and wide ranging list of customers which may be very attractive to some potential acquirers.

In summary, we believe that NeutraHealth has good prospects. Although there may be little to drive the share price too far in the short term. The shares are on a low rating and long term prospects appear promising.

the Group is focussing on organic growth

the shares trade on a

current year p/e of

just under 8

Written by Michael Crockett

Copyright Aimzine Ltd 2010

RETURN TO AIMZINE FRONT PAGE | February 2010

’

This article is the copyright of Aimzine Ltd. No part of the article should be copied, reproduced, distributed or adapted in any way without our prior consent. |