![]()

Companies that have been forced to issue profits warnings in recent months have seen their share price hit badly. Shares in NeutraHealth have been particularly harshly treated by the market following a negative Trading Update issued on 25 September 2008. This profits warning, coming two months after some fairly upbeat Interim Results, has prompted NeutraHealth’s house broker to sharply reduce their forecasts. However, NeutraHealth remains a profitable company with some valuable assets. On the face of it the share price fall is overdone with the Group now trading on a forward P/E of just over 3 on the downgraded forecasts.

I met with Finance Director, Robin Hilton to ask him about the downturn in the Group’s fortunes and to consider future prospects. Not surprisingly, Robin believes that the shares have been most unfairly treated by the market. We will consider Robin’s views and the Group’s valuation later but first I will introduce NeutraHealth and its products.

Nutraceuticals

NeutraHealth describes itself as a consolidator in the fragmented Nutraceutical market. The company produces and distributes vitamins, minerals and supplements, with its largest customers being Tesco and Boots for their own label products.

Since floating on AIM in 2005 the company has made five acquisitions, spending just over £25 million, such that now it is the third largest supplier (behind Seven Seas and Holland & Barrett) in the UK Vitamins, Minerals and Supplements (VMS) market.

The Companies and Their Brands

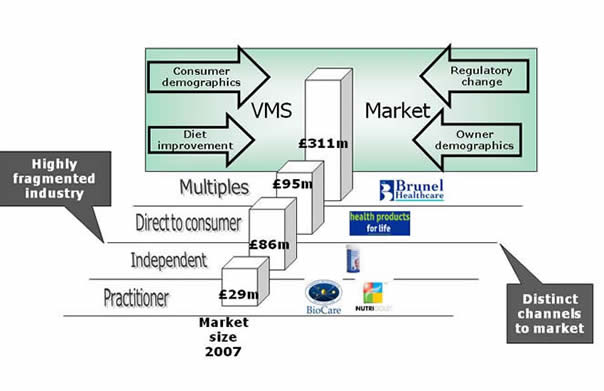

NeutraHealth has four distinct channels to market - Multiples, Direct to Consumers, Independent Retailers and Practitioner. This slide from a recent investor presentation shows these four channels – the brands marketed by the company are shown on the right of the slide.

|

The ‘Multiples’ channel represents over half of the company’s business although the higher margin, Independent and Practitioner, channels are also very important to the company.

To read more about NeutraHealth’s companies and brands see the company’s website here - . This gives information and website links for the Groups four operating subsidiaries

- BioCare

- Nutrigold

- Brunel

- Health Products for Life

![]()

![]()

Holford and Perrigo

There are 2 recent significant deals that we believe will have a considerable impact on the company over time.

- In July 2007 Neutrahealth announced a tie up with nutrition expert and best selling author, Patrick Holford – see the details here. The company has subsequently increased its marketing spend to promote the ‘Holford’ brand. Patrick Holford has a considerable following among nutrition conscious individuals and this 10 year deal could prove very important for the Group in the long term. Read more about Patrick Holford here.

- In July 2008 NeutraHealth acquired Perrigo UK Limited for £6.4 million. Perrigo were NeutraHealth’s biggest competitor in the Private Label VMS market. With the Perrigo acquisition comes a large state of the art manufacturing facility. This will provide significant synergy opportunities for the Group which had previously outsourced all packaging and manufacturing of products.

Acquisition Strategy

In total the Group has spent just over £25 million on its five acquisitions in the last three years. However, as the share price graph below indicates, the stock market puts a far lower value on the Group’s equity today. At the current share price of 2.6p the Group has a market capitalisation of just £4.6 million. Is the market being totally unreasonable? – we will look at this in Investment Considerations below.

The low share price does mean that it will be impossible for the company to complete any equity fund raising. Hence the Group’s acquisition strategy will have to be put on hold until the share price improves. We will now look at the reasons behind the latest share price fall.

Chilean Pilchards

On 25 September 2008 NeutraHealth issued a profits warning saying that the Group was suffering from the slowdown in consumer spending. Also, at the same time, it was facing growing cost pressures from such as plastics, Vitamin C and fish oil. Read the full Trading Statement here.

Robin Hilton described to me how quickly the Group’s outlook had changed. Up until June they had seen strong trading, but this had fallen away quickly thereafter. The cost pressures came partly from the increased oil price but also there were a number of exceptional increases elsewhere. For example, the company sources fish oil from Chilean pilchards and this year has seen an exceptionally poor harvest for pilchards in Chile.

In response to this deterioration in trading the Group’s house broker, Cenkos, revised forecasts downwards sharply. Cenkos reduced forecast turnover by 10% and profits by more than half. The table below shows these revised forecasts in context with the previous two years results.

|

Year to 31/12/06 |

Year to 31/12/07 |

Year to 30/12/08 (Forecast) |

Year to 30/12/09 (Forecast) |

Turnover (£,000) |

8,570 |

21,310 |

27,000 |

32,000 |

Pre-tax Profit (£,000) |

900 |

1,860 |

900 |

1,700 |

Earnings per share (pence) |

0.62 |

0.80 |

0.36 |

0.69 |

Robin Hilton says that sales have now stabilised at the reduced levels and that the cost pressures are showing signs of easing. He believes that the revised forecasts (above) are very conservative. Robin explained that, whilst they have seen a reduction in like for like sales, their business is likely to impacted much less than some other retail operations. Many of the users of Vitamins, Minerals and Supplements take these for medical reasons and those who buy VM&S for general health reasons tend to be from higher income groups. Such people are considered less likely to reduce their spend on products that are an important health benefit to them.

Shareholders

The largest shareholder in NeutraHealth is Bombay listed Elder Pharmaceuticals – see their website here. This company took a 21% stake in NeutraHealth when it purchased 37 million shares at 16p in July 2007. This subscription, at a 36% premium to the then NeutraHealth share price, was quite an endorsement for the Group. Elder are represented on the NeutraHealth board by non-executive director, Jagdish Kantisarup Saxena who is the founder and Chairman of Elder. Click here for a list of the other Major Shareholders.

There are five institutional investors listed, holding between 3% and 8% of the Group’s shares. However, now that the Group’s market capitalisation has fallen they are unlikely to attract further institutional support.

Of the directors non-executive director Sir Gulam Noon has the highest holding with 2.3% of the shares. The executive directors hold very few of the Group’s shares and with the share price so low it would encourage investors to see the executive directors increasing their holdings. NB The directors are entitled to share options but with the exercise prices ranging from 10p to 12.5p these have little value right now.

Investment Considerations

Judging what a share price should be in these markets is a pretty academic topic because, no matter how far below ‘fair value’ a share price may be, it can still get cheaper. NeutraHealth’s recent profit warning was unfortunate in its timing in that it followed fairly soon after optimistic Interim results and was issued at a time when the main markets of the world were ‘falling off a cliff’. The resultant fall whilst seeming harsh was to be expected in the circumstances.

NeutraHealth have built up an attractive group of brands in a lucrative and growing market for VMS products. The company has been profitable in its first 3 years and is forecast (on a conservative basis) to remain profitable, albeit with 2008 and 2009 forecast profits being lower than those achieved in 2007. Following the share price fall the company now trades on a forward (2009) P/E of just over 3 and has only limited debt. This low price indicates that the market has little faith in the company hitting forecast profits for 2008 and 2009. Yet the company believes that their broker’s forecasts are conservative.

To consider investing in NeutraHealth you would need to take a view on the future of the market in the UK for Vitamins, Minerals and Supplements. Certainly, if we were heading for a long and deep recession then we would be concerned that this VMS market could continue to contract in the short term. On the other hand if the recession were to be fairly mild then Robin Hilton’s view that there would be little further contraction would seem reasonable.

There is certainly considerable upside potential in these shares. If the company successfully navigates its way through this downturn and returns to a growth path then you would expect a P/E ratio of at least 10 to be justified. This would imply a potential trebling of today’s share price with a lot of potential for further growth.

NeutraHealth are likely to make a further trading update before the end of the year. We will comment on this and other NeutraHealth news in subsequent editions of Aimzine.

Written by Michael Crockett, Aimzine

The Group has spent

over £25 million on five

acquisitions in the last

three years and now

has a market capitalisation

of just £4.6 million